The European battle for gigafactories

€6.5 billion in investments and 5,500 jobs are at stake

Dear readers,

after our immersion in Japanese identity, back to Europe for a special issue. In February 2023, I published a study entitled "France in the European battle for gigafactories”. If you are in a hurry, this op-ed I wrote on fdi Intelligence, the Financial Times global investment website, is a good executive summary.

Today I'm publishing the 2024 edition of the study in which I take stock of the year 2023 and pinpoint the major industrial projects which should choose their location in Europe in 2024. You can find it below.

Guillaume

France in the European battle for gigafactories

While the Choose France summits have highlighted France's attractiveness for foreign industrial investment, the country has seen many large-scale projects slip through its fingers, such as Tesla or Intel. Today, France is all the more in need of hosting the next "mega-factories" to be set up in Europe, as it has become more de-industrialized than its European neighbours. This study aims to :

summarize France's successes and failures in setting up "mega-factories" in 2023,

detail the next 6 major industrial locations which should choose their location in Europe in 2024,

outline the measures in place to attract major industrial investments to France,

and propose new measures to improve France's attractiveness to mega-factories.

In this study, we define "mega-plant", gigafactory or large-scale foreign industrial investment as follows: an industrial project over €500m with majority foreign capital that is the subject of competition between countries to host it.

Summary

I. Review of the European industrial battles in 2023

A. The French victories

1. Prologium

2. Novo Nordisk

3. Holosolis

B. The French defeats

1. BYD

2. TSMC

C. Battles that never happened

1. Vinfast

2. Samsung

D. Summary table for 2023

II. 6 major industrial projects not to be missed in 2024

A. Moderna

B. Tesla

C. Skeleton Technologies

D. Alteo-Wscope

E. Umicore

F. The European plant of a Chinese manufacturer

G. Summary table: €6.5 billion of investment and 5,500 jobs at stake

III. How to win these projects

A. Measures have been taken...

1. The supply-side policy

2. The Green Industry Act

3. Choose France summits: French-style soft power

B. But France's attractiveness still needs to improve

1. Threats to supply-side policy?

2. Land, administrative simplification, training, a dedicated ministry: the battle for reindustrialization is still far from won.

3. Industrialists' concerns about making the most of the French nuclear fleet

Conclusion

I. Review of the European industrial battles in 2023

A. The French victories

1. Prologium

The Taiwanese manufacturer of new-generation batteries has chosen Dunkirk as the location for its €5.2 billion plant. The French port was competing with a site in the Netherlands and one in Germany. 3,000 jobs are expected to be created over the long term. This is a great victory for the Hauts-de-France Battery Valley, which is consolidating its position as a major centre for electric vehicles in Europe.

There are 5 main reasons for this success:

access to low-carbon, competitive electricity thanks to nuclear power ;

a battery industry ecosystem being created in the north of France (creation of dedicated training courses, establishment of upstream and downstream players in the battery value chain);

a €1.5 billion subsidy in several tranches up to 2029;

strong involvement and aggressive lobbying on the part of public players, from the French President to local councillors, not forgetting Business France and Nord France invest, who worked together to convince the company's directors to carry out the project in France;

the vice-chairman of Prologium is a Frenchman, formerly of Renault.

2. Novo Nordisk

In November, the Danish pharmaceutical giant announced that it will invest €2.1 billion to expand its Chartres plant. France was competing with Ireland to host this "pharmaceutical gigafactory". This is a major victory for France, which will enable to expand and secure a major pharmaceutical site, create 500 jobs and reduce the country's trade deficit.

I have analysed the statements made by several people involved in this issue (Novo Nordisk executives, specialist journalists, French authorities) and there seem to be 6 reasons for this choice, listed here from the most to the least crucial:

1. Novo Nordisk wanted to move quickly to increase its production capacity in response to the explosion in global demand for anti-obesity and anti-diabetes products, and expanding an existing site is quicker than building a new one. Apart from Denmark, where it has just announced a €6bn investment in its historic site, Chartres is the company's only other European site;

2. the government's pro-business policy (lower production taxes, lower corporation tax and reform of the labour market) reassured the Danish company that the site would be competitive in the long term and that the investment would be profitable;

3. Decarbonised electricity thanks to nuclear power: the CEO of Novo Nordisk emphasised this crucial point, as the company is very committed to the energy transition and is aiming for carbon neutrality by 2045;

4. the very strong lobby from the President of the Republic and Bercy: Novo's CEO was in direct contact with the President and took part in the Choose France summit in May 2023. He praised the responsiveness of the French authorities in bringing the project to fruition quickly;

5. France's geographical position, well placed to serve the European market;

6. and the reforms underway to reduce the time it takes to bring medicines to market in France and to set prices. But this is not the most important factor, as the plant is designed for export.

More generally, the trend in foreign investment in the pharmaceutical industry in France has been positive in recent months, with several major announcements: These include Novo Nordisk (€2.1bn), GSK (€350m), Lilly (€160m) and Pfizer (€1bn in R&D). Germany is also in the running ($2.5bn invested by Lilly).

3. Holosolis

In May 2023, the European consortium Holosolis announced that it would invest €710m to build one of Europe's largest photovoltaic cell and panel factories in Hambach, in Eastern France. 1,700 jobs are expected to be created. This is a crucial investment: 90% of the panels installed in Europe are imported from China. With an annual output of 5 gigawatts, this plant will be able to equip one million European homes a year.

Several European sites were competing. The French site was chosen in part because it is a turnkey industrial site. A previous photovoltaic panel factory project for which the site had been serviced and prepared was finally cancelled. The site was therefore available for a new project "that wanted to move quickly".

Public consultation is underway and work is due to start this summer.

B. The French defeats

1. BYD

Chinese carmaker BYD, the world's leading manufacturer of electric vehicles ahead of Tesla, has chosen Hungary as the location for its future European plant. France was in the running, alongside Germany, Spain, Poland and the Magyar winner. Bruno Le Maire, French finance minister, travelled to Shenzhen in August to meet BYD's CEO and try to convince him to build the plant in France. It was not enough.

With France's automotive trade deficit set to reach €20 billion by 2022, this plant was an opportunity for France to repeat the success of Toyota's move to Valenciennes in 2001. The Japanese manufacturer's plant has since become France's leading automotive site in terms of the number of vehicles produced, and the majority of its output is exported.

Winning the BYD plant would also be an opportunity to make up for Tesla's failure: Elon Musk's European gigafactory, which moved to Berlin in 2019, already employs 11,000 people. The size of BYD's Hungarian plant could be close to that of the American manufacturer's German plant.

2. TSMC

Although the decision was already in the air, it wasn't until August 2023 that TSMC made it official that it would be setting up its first European plant in Dresden, in eastern Germany. The Taiwanese chip giant will invest €10 billion and create 2,000 jobs. The worst thing about this deal is that France does not seem to have been seriously considered as a location. Thanks to its critical mass, Silicon Saxony, the microelectronics cluster around Dresden, now dominates the European semiconductor landscape: TSMC has set up there, among other reasons, because it can find the suppliers it needs there.

While STMicroelectronics and GlobalFoundries are investing €8 billion near Grenoble, our neighbour across the Rhine has invested €50 billion over the past 3 years (Intel, TSMC, Wolfspeed, Infineon, etc.), a ratio of 1 to 6. When it comes to chips, Germany is in the driving seat.

C. Battles that never happened

1. Vinfast

I have to admit that I got a bit carried away with the Vinfast dossier. Although Olivier Becht, the former Minister Delegate for Foreign Trade and Economic Attractiveness, did meet the Vietnamese manufacturer's directors during a trip to Asia in March 2023, Vinfast will not be setting up a factory in Europe for several years. The company has just started work on its American plant, but for the time being it will be content to export its cars from its Vietnamese plant to the European market. The Vietnamese manufacturer has also just announced a $2 billion investment to build a plant in India.

2. Samsung

As with Vinfast, I pointed out in last year's review that the Korean electronics giant, like its competitors, was considering the possibility of building a factory in Europe. If the project is not cancelled, it will not happen immediately. As revealed in June 2023 by the Korean business monthly BusinessKorea, Kyung Kye-hyeon, head of Samsung's semiconductor subsidiary, visited several European regions, including Munich and Stuttgart in Germany, Geneva in Switzerland, Amsterdam in the Netherlands and Tel Aviv in Israel, to discover the local ecosystems. However, Samsung will not be building a factory in Europe in the short term. The company is already in the process of investing tens of billions of dollars to build semiconductor plants in Korea and the United States, and prefers to put its European plans on hold.

D. Summary table for 2023

France's results in 2023 in the competition for major industrial sites in Europe are mixed.

On the one hand, the trend is more positive than in previous years, with France winning more and more decisions on major projects. Of particular note is the mobilisation to win the Prologium, Novo Nordisk and Holosolis cases.

On the other hand, the defeat in the BYD and TSMC cases is a black mark on the picture, as these were the two most significant announcements of the year in Europe. No less than the world's No. 1 manufacturer of electric cars and the world's No. 1 chipmaker announced their first European plant this year, and neither chose France. What's more, these are new plants, unlike Novo Nordisk, which is an extension of an existing site.

There is also a risk factor to take into account: while BYD, TSMC and Novo Nordisk are well-established global industrial leaders, Prologium and Holosolis are young companies that have never yet built large-scale plants.

I produced a summary table of projects to conclude my study last year: here is the updated version.

I would add that it would have been artificial to add to this list the investments announced in 2023 by XTC/Orano in Dunkirk (€1.5bn for a battery components plant) and Carbon in Fos-sur-mer (€1.5bn for a solar panel plant): as far as the first project is concerned, there is nothing to indicate that Dunkirk competed with other European sites, and as far as the second is concerned, it is a French-owned company whose 3 shortlisted sites were located in France (no European competition).

2024 will be a busy year for major industrial sites in Europe: let's take a look at the 6 sites for which France is in the running.

You will also find a summary table for 2024 at the end of the following section.

II. 6 major industrial projects not to be missed in 2024

Several foreign companies have announced their intention to set up a plant in Europe requiring an investment of over €500 million. Among the most important projects, here are the next 6 plants that could be announced in 2024 and that France is competing for.

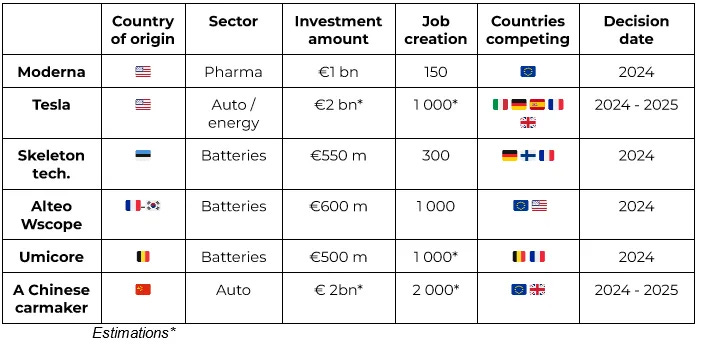

A. Moderna

This is a project that has been under discussion for several months and that I had already included in my study last year: the American company is in discussions with several European governments about setting up an ANRm technology plant in a European Union country. This is an opportunity for France to catch up: in June 2022, Moderna announced its first European plant in the UK, capable of producing 250 million doses of vaccine a year. 150 highly qualified jobs will be created. The laboratory will invest £1.1 billion, thanks to the British government's commitment to buy vaccines from Moderna for 10 years.

The latest news (interview with Stéphane Bancel, Moderna's French CEO, on BFM TV in September 2023, a French TV channel) is that Moderna intends to build its first EU plant in France. The CEO announced that Moderna had made a proposal to the French government. Negotiations are still underway, as Moderna would like the French government to commit to buying the plant's production over the long term, as it has done in the UK. This media appearance by the American company's CEO is therefore a way of putting the ball (and the pressure) in the government's court. The investment is estimated at €1 billion, and the project is "in advanced discussions with the French government", as Sandra Fournier, Director of Moderna France, told L'Usine Nouvelle in September 2022. This plant is crucial to French and European sovereignty in vaccines.

Negotiations between Moderna and the French government are likely to be tough, because while the US company's turnover has risen from $60m in 2019 to $19bn in 2021, it has fallen back to $6bn in 2023, following a drop in sales of vaccines against covid.

B. Tesla

Bruno Le Maire, the French finance minister, confirmed in June that discussions were underway and that several options were on the table. Elon Musk's presence at the latest Choose France summit in May 2023 and at the Vivatech trade fair in Paris in June 2023 would seem to confirm the Tesla boss's interest in France. On the occasion of the latter visit, he said that it was "very likely that Tesla will do something very important in France in the years to come". But be careful not to over-interpret: Elon Musk deliberately keeps things vague and regularly meets world leaders to discuss potential industrial investments (Italy, India, etc.). Nevertheless, this would be an opportunity for France to make up for the failure of 2019 when Tesla chose Berlin for its European gigafactory.

Although little is known about Tesla's next investments in Europe, 4 options are said to be on the table according to various articles in the European specialist press:

a car assembly plant to complement the Berlin Gigafactory. Tesla would like a second European factory, and the Spanish press has revealed that Valencia is on the shortlist, along with the UK, Italy and France;

an battery factory ;

a megapack factory (an energy storage station made up of several high-power batteries), via its subsidiary Tesla Energy. Tesla already has a megapacktory in the United States and has just launched the construction of a similar plant in China;

a solar panel factory, via its subsidiary Tesla Energy. It's not widely known, but Tesla is also a manufacturer of solar panels. France could be the site of a factory dedicated to the European market.

C. Skeleton Technologies

Skeleton Technologies is an Estonian company that produces high-power batteries used in transport (trains, trucks) or energy storage. The industrial start-up has raised €300m, has its first factory in Germany and counts Siemens among its shareholders and customers.

The company is now preparing to choose the location for its future €550 million European plant. 3 countries are on the shortlist: Germany, Finland and France. The sites under consideration in France are located in the Hauts-de-France region: if the decision is taken, it would be a new production site for the battery valley. The decision will be based on a number of criteria, including the price of land and energy, subsidies, and the presence of an ecosystem around the battery, as the company wants to attach an R&D centre to the factory.

Skeleton's CEO took part in the last Choose France summit, and last October he accompanied the Estonian Prime Minister on a trip to Paris on the theme of Franco-Estonian economic cooperation.

D. Alteo-Wscope

In November 2022, French alumina supplier Alteo and South Korea's Wscope announced plans to invest €600m in the Hauts-de-France region to build a plant to produce separator films (key battery components located between the cathode and anode) for electric batteries. The plant is intended to supply future battery gigafactories in the Hauts-de-France region. The location was to be announced in the following months, but there has been no news from the companies involved in the project for a year. According to the regional press, Valenciennes is one of the sites being considered, but it is in competition with foreign sites, particularly in the United States.

E. Umicore

Umicore, the Belgian materials company, is wavering between northern France and Belgian Flanders as the location for its future European plant for recycling electric car batteries.

The lack of manpower and land in Belgian Flanders and the length of administrative procedures could lead the company to choose France for this €500 million investment. Another crucial factor is the level of subsidy. The Flemish regional government has promised Umicore a subsidy of €55 million if the company decides to build the plant in Antwerp or Zeebrugge, i.e. 10% of the cost of the project. Yet France does not hesitate to offer subsidies representing 20 to 30% of the cost of a project. For example, the European Commission authorised the French government to pay a subsidy of €1.5 billion to the Taiwanese manufacturer to set up its first European battery factory in Dunkirk (Nord).

The Belgian manufacturer was due to make its decision at the end of 2023.

F. The European plant of a Chinese manufacturer

I'm not happy about the rise of Chinese carmakers: BYD, for example, has announced that it wants to "destroy the old legends of the automobile", targeting European brands in the process. I hope to see Renault succeed in its audacious industrial gamble: by creating the Electricity industrial cluster, Renault aims to produce 1 million electric vehicles in the north of France by 2030 (I talk about it here).

But I'm a pragmatist: just as Japanese and Korean manufacturers have done, Chinese manufacturers are going to make their mark on the European market. After the failure on the BYD case, France needs to win back one of these future production sites to avoid widening its automotive trade deficit. I'm thinking in particular of the 3 manufacturers who have announced their intention to build a plant in Europe: SAIC MG, Chery and Great Wall Motors.

The magazine Challenges recently revealed that the Chinese electric car manufacturer SAIC, which owns the famous British brand MG, could build its European plant in Eastern France, on the former Smart site at Hambach. But the competition is fierce: Spain, the UK, Germany and Italy are also in the running.

Chinese manufacturer Chery also wants 2 plants in Europe: one in the UK and one in the European Union. Spain, Germany, Romania, Italy and France are in the running. According to the Spanish press, the Chinese manufacturer is targeting the site of the former Nissan factory in Barcelona. A decision on the site is said to be imminent.

The third Chinese manufacturer interested in setting up a production site in Europe is Great Wall Motors. But France does not appear to be under consideration for the moment: the 3 countries under consideration are Germany, the Czech Republic and Hungary, according to a specialist European media outlet.

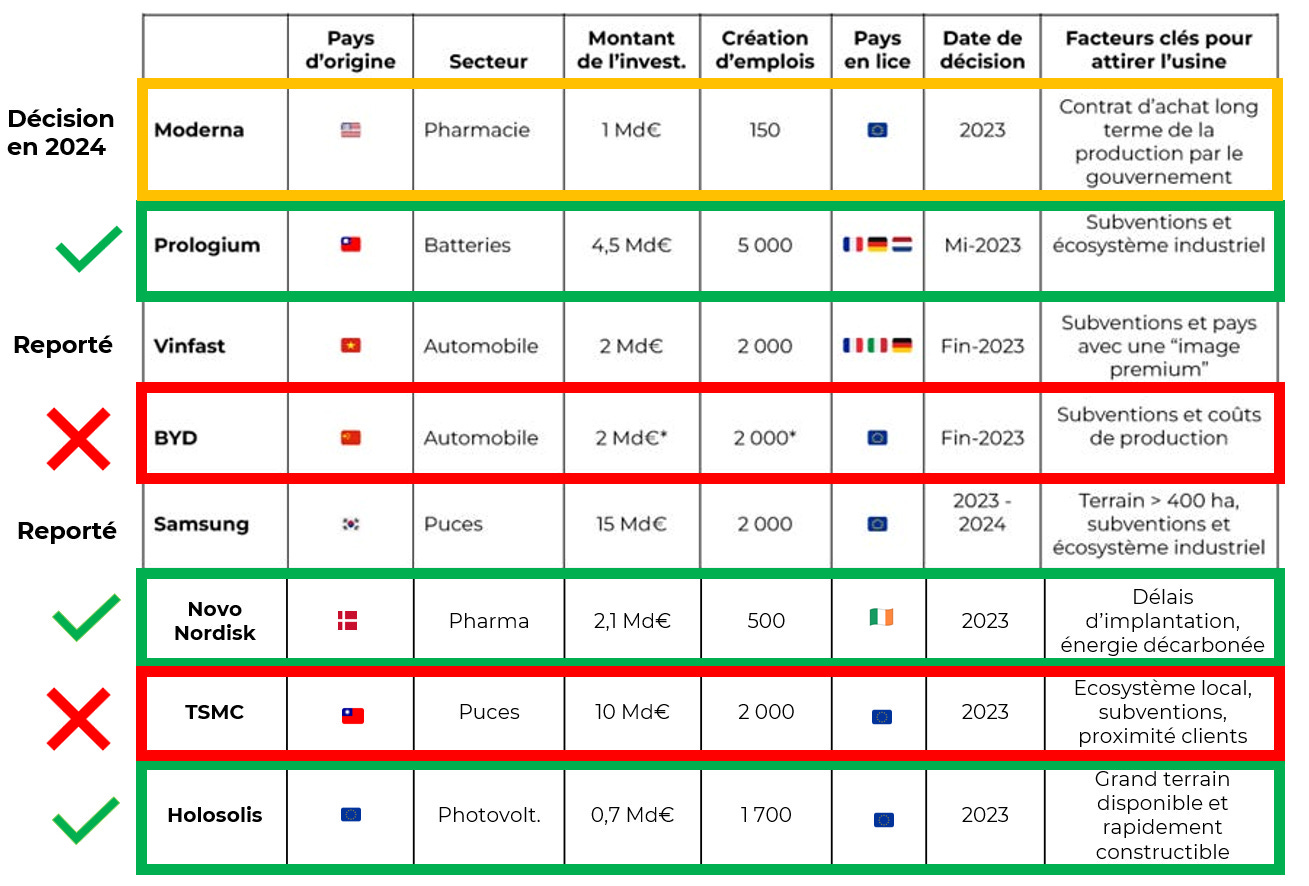

G. Summary table: €6.5 billion of investment and 5,500 jobs at stake

These 6 major industrial projects, the location of which should be decided in 2024, represent over €6.5 billion of investment and almost 5,500 jobs.

While certain levers are not in the hands of the government and local authorities, such as the presence of a pre-existing industrial ecosystem, public action can be decisive on a number of levels:

availability of large plots of land that can be built on quickly ;

the amount of subsidies ;

a well-trained workforce ;

and decarbonised, competitive electricity.

III. How to win these projects

Let's now look at the measures that have been and will be taken to attract these major industrial projects. We will see that while recent reforms have improved the country's attractiveness, not everything is yet in place to give us the means to win major industrial projects.

A. Measures have been taken...

1. The supply-side policy

The choice of a site for an industrial project is based on qualitative criteria (availability of land, infrastructure, quality of workforce, local ecosystem, relationship with public authorities, etc.) and quantitative criteria (level of subsidies, energy prices, cost and availability of workforce, level of taxation). The major groups have teams dedicated to new industrial projects: they analyse and compare each component of a country's attractiveness. Price competitiveness is one of the fundamental dimensions.

In the various comparative studies (or benchmarks) used by manufacturers, France's situation has improved overall in recent years, thanks in particular to reforms that are part of the "supply-side policy":

Corporate tax rate reduced from 33% to 25% between 2017 and 2022;

reduced labour costs (CICE reform);

a €18bn cut in production taxes;

labour market reforms ;

and the recent reform of the vocational lycée, one of the aims of which is to address labour shortages in industry.

2. The Green Industry Act

The year 2023 saw the passing of the Loi industrie verte (Green industry act), which improved France's situation in an area where it was lagging behind: the time taken to set up industrial sites. The report entitled "Simplifying and accelerating the establishment of economic activities in France", submitted to the government in March 2022, showed that the average time taken to set up a factory was 8 months in Germany and 17 months in France.

The Green Industry Act has provided some initial responses. In particular, I would highlight 2 measures concerning large-scale industrial facilities:

simplification of the environmental authorisation procedure to speed up the process of setting up new plants. Examination by the departments and by the environmental authority and public consultation will be carried out in parallel. The aim is to halve the time taken to issue authorisations, from 17 months today to nine months tomorrow;

the creation of an exceptional simplified procedure for industrial projects of major national interest, enabling local town planning documents and regional planning documents to be brought into line more quickly, accelerated electricity connection procedures and the issuing of building permits by the State rather than by local authorities. This exceptional procedure will apply to projects for very large plants (gigafactories), which will be identified by decree.

At the same time, in response to the US IRA (inflation reduction act), the Finance Bill for 2024 introduces a green industries investment tax credit (C3IV) to attract industrial investment in wind power, photovoltaics, batteries and heat pumps. This was certainly a decisive factor in convincing the French group Atlantic to invest €150 million to build its new heat pump factory in Burgundy rather than in Poland.

3. Choose France summits: French-style soft power

The Choose France summits are proving to be an offensive and effective soft power tool, and it's The Economist that says so. In an article published in November 2023, the weekly explains that these summits in Versailles are an asset for France when it comes to winning major international industrial projects. When a CEO is hesitating between 2 countries for an investment project, face-to-face meetings with the President and the ministers concerned, assuring him that the authorities will support his project on all fronts (regulatory, financial and speed of execution), can tip the balance in the right direction.

In his November 2023 report Boosting foreign direct investment in the UK for the UK Treasury, former UK MP Richard Harrington also praises this soft-power policy, which seems to be winning over international investors: "A number of senior business representatives who spoke to the Review reported that their CEOs and Presidents were used to receiving texts directly from President Macron, being invited to the Palace of Versailles and having ‘the red carpet rolled out’. Investors reported that this type of relationship-building was an important element in their investment decision-making, taken as an indication of the level of commitment the UK government has to investment partnerships. An international conglomerate with a net worth of over $300 billion operating in over 150 countries said relationships were ‘critical’ to how they do business”.

Choose France is beginning to be identified as an important international business summit: I think that this tool should be maintained, even in the event of a political changeover.

B. But France's attractiveness still needs to improve

1. Threats to supply-side policy?

In an interview with Les Echos at the end of December 2023, Louis Gallois, whose eponymous 2012 report marked the beginning of the supply-side policy in France, warned of the very bad signal sent to industry by the reduction in tax relief on salaries from 2.5 to 3.5 SMIC (the minimum wage) enacted in the 2024 budget. This extra burden will weigh disproportionately on industry, which pays the highest salaries (above 2.5 SMIC): although it accounts for 10% of GDP, industry will pay 20% of the total amount of this cut in tax relief, or €140 million a year according to Louis Gallois. These recent decision can only worry French manufacturers. Meanwhile, the coalition in power in Germany has just decided to cut corporate taxes by €32 billion over 4 years, and the UK government has announced a €9 billion annual tax allowance on business investment.

Let's not forget that France is still a country that overtaxes its production base. Taxes on production remain at a very high level: after taking into account the new cuts in 2023 and 2024, the gap will remain around €30bn compared with the EU27 average and €60bn compared with Germany. The abolition of the Contribution de solidarité des sociétés (C3S) (€4bn) should be a priority: it has been described by the Conseil d'analyse économique (CAE) as "the most harmful tax to be abolished as a matter of priority". This tax on turnover "reduces the competitiveness of businesses, acting as a tax on exports and a subsidy on imports". According to the CAE, abolishing it could improve the manufacturing trade balance by €5 billion.

2. Land, administrative simplification, training, a dedicated ministry: the battle for reindustrialization is still far from won.

In his report on attractiveness submitted to the Prime Minister in December 2023, MP Charles Rodwell stresses the importance of legal certainty for investments. In the course of his work, the MP has, for example, "been confronted with dozens of situations, some of them bizarre, in which the administration's 'changes of foot' regarding the application of a standard or a decision have led to the abandonment of a project to set up or develop a business by French or foreign investors," says the report. It proposes extending the business location contract introduced in the Hauts-de-France region in 2017. In practical terms, this would consist of a contractual commitment between the State, the region and the host conurbation, for a period of five years, to provide investors with security in the development of their location or expansion project, within a pre-defined, stable and guaranteed legal framework (total stability of the local and national regulations applicable to the project, for a period of five years from the signing of the contract).

A law dedicated to administrative simplification, could give concrete form to these proposals in the first half of 2024.

The question of land is also a fundamental issue when it comes to attracting major industrial sites. Tesla and Intel set up in Germany partly because France was unable to offer large plots of land that could be built on quickly. France must not miss out on the next Tesla or MG/SAIC plant for this reason.

The "turnkey industrial sites" scheme has helped to speed up a number of sites, but land availability is not always up to date and France still does not have a sufficient stock of large plots of land that can be built on quickly. The government relaunched a survey of industrial sites in the autumn because of the urgency of the situation: a recent study estimated that France needs 20,000 hectares of industrial land by 2030 if it wants to re-industrialise.

To give concrete administrative form to the central role given to industrial policy, economist Christian Saint-Etienne proposes the creation of a powerful Ministry of Reindustrialisation, which would also be responsible for energy policy, innovation and vocational training. The recent attachment of energy to Econony minister is a first step.

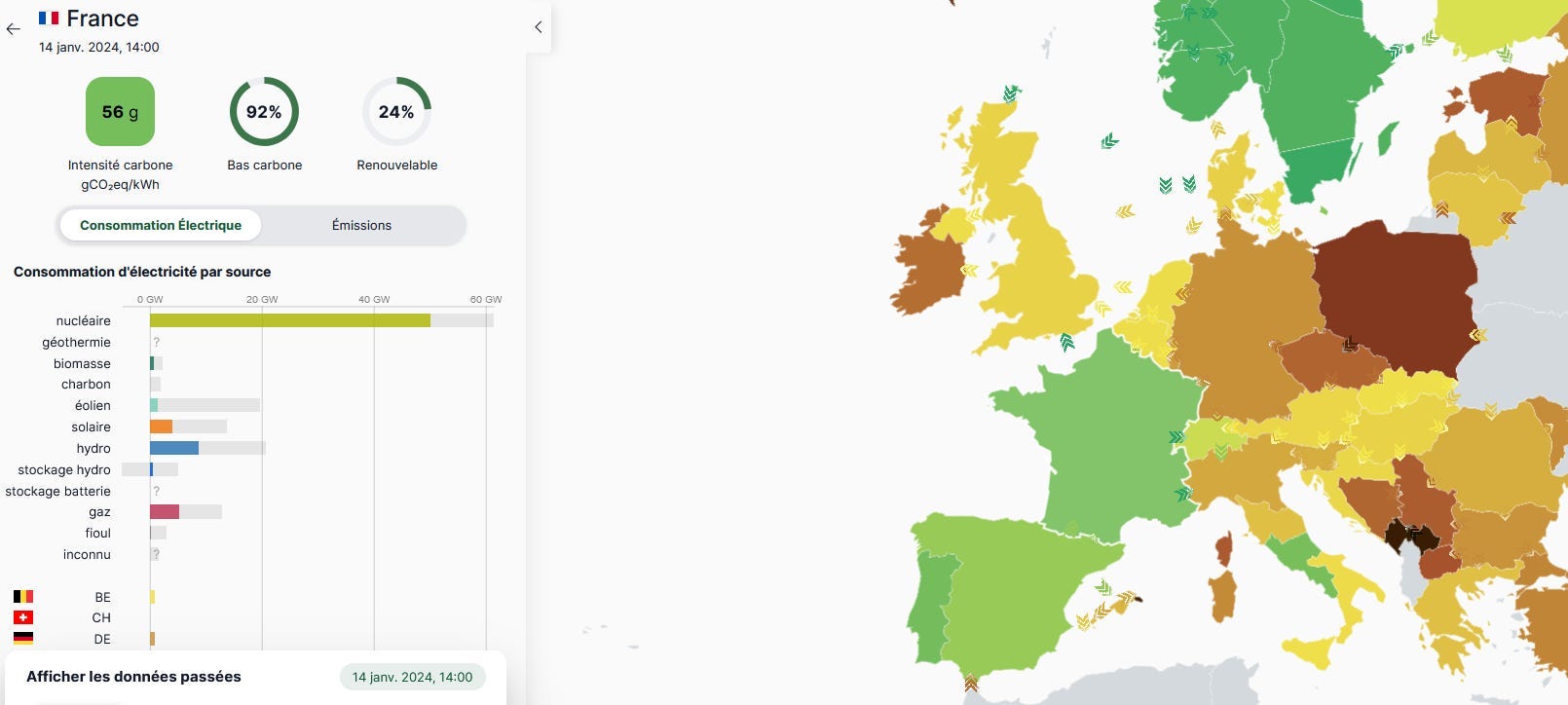

3. Industrialists' concerns about making the most of the French nuclear fleet

At a time when carbon intensity is becoming a purchasing criterion for consumers and the price of energy is a key factor in investment decisions, France's electricity is among the most carbon-free (53 compared with 414 gCO2eq/kWh for Germany) and competitive in Europe in terms of production costs, thanks to nuclear generation. However, the agreement reached between the French government and EDF in October 2023 concerning the setting of electricity prices from 2026 onwards is a cause for concern for French industry. CLEEE, an association of energy-intensive companies, is denouncing "a major step backwards for French businesses": it anticipates a doubling in the average price of electricity compared with the current situation. What's more, the mechanism resulting from the agreement is designed in such a way that electricity prices in year n will only be known in year n+1 (retrocession mechanism), which means a loss of visibility for businesses, complicating investment decisions and budget planning.

Although Finance Minister is planning specific measures and encouraging the signing of long-term contracts between electricity-intensive industries or large-scale consumers and EDF, we will have to wait for the draft law intended to materialise the agreement between the State and EDF (1st half of 2024) to see more clearly.

Conclusion

After a mixed 2023 in terms of mega-plant locations in France, 6 major industrial projects representing €6.5bn of investment and 5,500 jobs will choose their location in Europe.

Attracting these mega-factories is part of the battle for reindustrialisation, which is still far from won: the weight of manufacturing industry in GDP in France has continued to fall, to 9.5% in 2022, compared with 14.8% in the eurozone and 18.4% in Germany.

These 6 projects are representative of the key industries of the coming decades: mRNA vaccines, batteries and electric vehicles. Attracting them would enable France and Europe to position themselves in the industries that will ensure our sovereignty and prosperity in 2030 and 2040.

Attracting 3 of these 6 projects would be a very good result for France:

we can be optimistic about the Moderna factory: the company has stated that it wants to build its European factory in France and is awaiting a response from the government;

Attracting Skeleton Technologies, Umicore and Alteo-Wscope would strengthen the ecosystem of the Battery Valley in northern France;

Repeating the success of Toyota Valenciennes (the Japanese carmaker built a plant in northern France in 2001) by winning a Chinese car plant would consolidate French car production and reduce the automotive trade deficit, which has reached €20 billion by 2022;

Finally, attracting a Tesla plant would be a prestigious victory, as Elon Musk's company is at the forefront of electric cars.

I also hope that many projects have slipped under my radar. We'll see if the next Choose France summit, due to be held in March 2024, brings any good news...

Study published in collaboration with the Le Millénaire think tank.